Estimate Your Mortgage Payment Easily

- Ryan Daly

- Jun 16, 2025

- 4 min read

Understanding how much you will pay each month for your mortgage is essential when purchasing a home. It's not just about the house price; you must also factor in interest rates, insurance, tax, and down payments. Luckily, estimating your mortgage payment doesn't have to be complex. With a mortgage payment calculator, you can simplify the process and make better financial decisions.

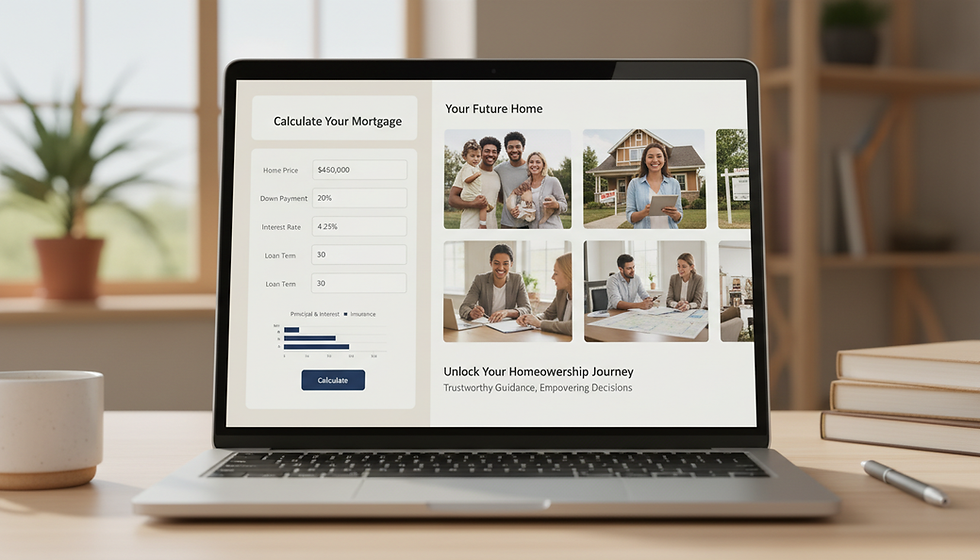

What is a Mortgage Payment Calculator?

A mortgage payment calculator is a tool that estimates how much your monthly mortgage payment will be based on several key factors. By inputting information about the loan's value, interest rate, and loan term, you can get a glimpse into your future payments.

Most calculators will also factor in property taxes and insurance, giving you a more accurate picture of what to expect. They are user-friendly and typically require only a few pieces of information.

How to Use a Mortgage Payment Calculator

Using a mortgage payment calculator is straightforward, but knowing what inputs to use is essential for accurate results:

Home Price: Start with the total price of the home you want to purchase.

Down Payment: Input your planned down payment amount. This is typically a percentage of the home price.

Loan Term: Decide on the loan term, usually ranging from 15 to 30 years.

Interest Rate: Use the prevailing interest rate for mortgage loans. This can vary significantly, so checking current rates is essential.

Property Taxes and Insurance: Include estimated costs for property taxes and homeowners insurance. These can vary by location.

Once you've entered all your information, the calculator will provide an estimate of your monthly payment. This will help you budget accordingly and understand whether the home fits within your financial parameters.

Factors Influencing Your Mortgage Payments

Several factors can influence your mortgage payments, and understanding them will help you estimate more accurately:

Interest Rate

The interest rate is perhaps the most critical factor. Even a small change can lead to significant differences in your monthly payment. For example, on a $250,000 loan with a 30-year mortgage, a 0.5% increase in interest can raise your monthly payment by over $70.

Loan Term

The length of your mortgage term greatly affects your payment. Longer terms generally result in lower monthly payments but higher overall interest paid. A 30-year loan spreads payments over a longer period, while a 15-year loan generally has higher payments but saves on interest costs.

Down Payment

Generally, making a larger down payment reduces your monthly payment. For example, a 20% down payment will lower the loan amount and may help eliminate private mortgage insurance (PMI), further reducing your payment.

Property Taxes and Homeowners Insurance

These additional costs can significantly affect your monthly budget. Be sure to include accurate estimates for both in your calculator. These costs vary by location and property value, so local research is immensely helpful.

Helping You Make Informed Decisions

Having an accurate mortgage payment estimate is crucial for making informed financial decisions. For instance, knowing what your payments will be can help you compare different properties and negotiate better during the purchase process.

Many buyers overlook the long-term costs, focusing only on the purchase price. Underestimating monthly payments can lead to financial strain later. Therefore, using a mortgage payment calculator is not just about getting a number; it's about understanding your financial future.

Tips for Choosing the Right Mortgage

When applying for a mortgage, consider these helpful tips:

Research Different Loan Options

There are different types of mortgage loans available, including fixed-rate, adjustable-rate, FHA, VA, and others. Compare all options thoroughly. Each type has its pros and cons, depending on your situation.

Shop Around for Interest Rates

Don’t settle for the first offer you receive. Check multiple lenders to find better rates and terms. Even a small difference in interest can generate substantial savings over the life of the loan.

Get Pre-Approved

Before house hunting, getting pre-approved can streamline the buying process. It gives you a clear idea of your budget and shows sellers that you are a serious buyer.

Consider Additional Costs

Always remember to factor in additional costs like closing costs, maintenance, and potential homeowner association fees. These expenses can vary greatly between properties and can affect your overall budget.

Taking the Next Steps

Once you have your estimated mortgage payment from a calculator, it's time to take action:

Determine Affordability: Review your budget to see if you can comfortably manage the estimated payment alongside your other expenses.

Consult a Financial Advisor: If you have reservations, consulting with a financial advisor can provide tailored advice and planning.

Inquire about Incentives: Many lenders offer promotions or assistance programs; ask about first-time homebuyer incentives or assistance.

Estimating your mortgage payment can seem intimidating, but it doesn't have to be. With the help of tools like a mortgage payment calculator, you can simplify the process and make informed home-buying decisions.

Adopting a careful approach to your financial commitment can set you on the path to homeownership without undue stress. Happy house hunting!

Comments